Table of Contents

- 1. Who qualifies for the regime forfettario in 2026?

- 2. The 5% vs 15% flat tax: which rate applies to you?

- 3. ATECO profitability coefficients

- 4. INPS contributions: the hidden cost

- 5. Net income calculator: real numbers at every revenue level

- 6. Forfettario vs regime ordinario: which saves more?

- 7. Tax payment calendar: when do you pay?

- 8. Frequently asked questions

You've heard the pitch: open a Partita IVA under the regime forfettario, pay a flat 15% tax, keep most of what you earn. It sounds almost too good for a country with a reputation for heavy taxation.

The reality is more nuanced — but still genuinely good, if you understand the full picture. The forfettario does offer one of the lowest effective tax rates available to self-employed workers anywhere in Europe. The catch is that the INPS social contribution — Italy's pension and social security levy — sits on top of the flat tax and is something many guides barely mention. Miss it, and your net income calculation will be wrong by thousands of euros.

This guide gives you the complete 2026 picture: who qualifies, how the flat tax is actually calculated, what INPS costs at every income level, and how the forfettario compares to the standard regime ordinario. Real numbers, not approximations.

1. Who qualifies for the regime forfettario in 2026?

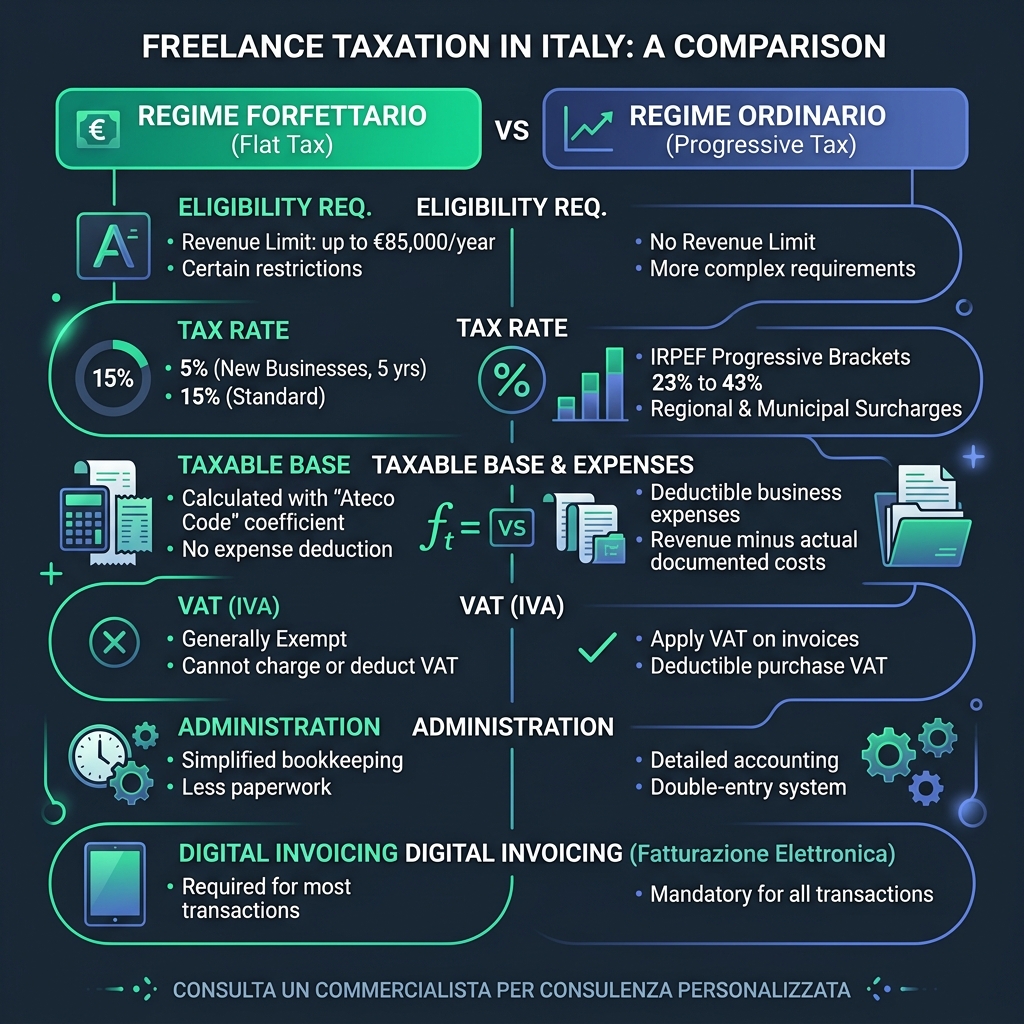

The forfettario is a simplified flat-rate tax regime available to individual self-employed workers and sole traders (Partita IVA). To access it in 2026, you must meet all of the following conditions.

Revenue cap: €85,000 per year. Your total annual revenue — not profit, but total invoiced income — must not exceed €85,000. This cap was raised from €65,000 to €85,000 in 2023 and remains at that level in 2026. If you exceed it during the year, you exit the regime from the following fiscal year. If you exceed it by more than 50% (i.e. you invoice over €127,500 in a single year), you exit immediately mid-year.

No employment income above €30,000. If you also hold a salaried employment contract alongside your freelance work, your gross employment income must not exceed €30,000. If it does, you cannot access the forfettario regardless of your freelance revenue.

No majority ownership in partnerships or companies. You cannot be a controlling partner in an SRL, SNC, or SAS that operates in the same business sector as your Partita IVA activity.

No former employer rule (first two years). If you leave a salaried job and immediately open a Partita IVA providing services to your former employer, you are barred from the forfettario for the first two years. This rule targets disguised employment.

Non-resident rule for income source. More than 75% of your revenue must come from Italian clients or from foreign clients where the services are performed in Italy. Freelancers billing exclusively to foreign clients may face complications with this requirement and should verify with a commercialista.

If you meet all these criteria, the forfettario is almost certainly your optimal regime in 2026 — especially in the early years of activity when the 5% startup rate applies.

2. The 5% vs 15% flat tax: which rate applies to you?

The forfettario charges one of two flat tax rates depending on how long your business has been operating.

- 5% for the first five years of a new business activity, provided you have not held a Partita IVA in the preceding three years and the activity is genuinely new rather than a continuation of a previous business or employment. This startup discount makes the forfettario extraordinarily attractive for new freelancers: five years of paying roughly half the standard rate.

- 15% from year six onwards (or from year one if you do not meet the startup conditions). This is the standard forfettario rate and is the figure most guides refer to when describing the regime.

The tax is applied not to your actual revenue but to a reduced "deemed income" figure calculated using your sector's profitability coefficient. The coefficient is the element most people miss and the reason your effective tax rate on gross revenue is always lower than 5% or 15%.

3. ATECO profitability coefficients: the number that determines your taxable base

Under the forfettario, the government does not ask you to track or prove your actual business expenses. Instead, it applies a standardised profitability coefficient based on your ATECO activity code. This coefficient represents the assumed profit margin for your type of business. You pay tax only on that assumed profit — not on total revenue.

The key coefficients for 2026:

| Business category | ATECO examples | Coefficient |

|---|---|---|

| Professional & technical services | Consultants, lawyers, architects, accountants | 78% |

| IT & software | Developers, data analysts, SaaS | 67% |

| Trade & commerce | Retail, wholesale, e-commerce | 40% |

| Food & hospitality | Restaurants, bars, catering | 40% |

| Construction & crafts | Tradespeople, contractors | 86% |

| Other services | Freelance writers, designers, tutors | 67% |

| Agriculture | Farming activities | 25–40% |

How this works in practice: a software developer with a 67% coefficient who invoices €50,000 in 2026 has a taxable base of €50,000 × 67% = €33,500. The 15% flat tax applies to €33,500, not to €50,000. Tax owed: €5,025.

A management consultant with a 78% coefficient who invoices €50,000 has a taxable base of €39,000. Tax owed at 15%: €5,850.

The lower the coefficient, the lower the taxable base — which is why traders and food businesses benefit disproportionately from the forfettario despite often earning less than professionals.

4. INPS contributions: the hidden cost most freelancers miscalculate

The flat tax is only half the story. Every forfettario freelancer also pays INPS social contributions — Italy's pension and social security system. This is the figure that most English-language guides understate or omit entirely.

The contribution you pay depends on your professional category, not your ATECO code.

- Gestione Separata (most freelancers and knowledge workers): 26.07% of your net taxable income (i.e. the coefficient-reduced figure). This applies to consultants, IT professionals, writers, designers, lawyers, architects, and most other knowledge-work categories who are not enrolled in a specific professional fund (cassa professionale).

- Artigiani e Commercianti (tradespeople and traders): a fixed minimum contribution of approximately €4,200 per year regardless of income, rising proportionally above a threshold. This is more complex and depends on your specific INPS category.

- Professional funds (casse professionali): doctors, engineers, accountants, notaries, and certain other regulated professions are enrolled in their own sector-specific pension funds with different contribution rates, typically 10–16%.

For the majority of freelancers — those in Gestione Separata — the INPS calculation in 2026 is:

Taxable base (revenue × coefficient) × 26.07% = INPS contribution owed

Using the developer example: €33,500 × 26.07% = €8,733 in INPS contributions.

Add that to the €5,025 flat tax: total deductions = €13,758 on €50,000 revenue. Net income: €36,242, an effective rate of approximately 27.5% on total revenue.

This is still substantially lower than what a salaried employee earning €50,000 gross would net under IRPEF — but it is meaningfully different from the "I only pay 15% tax" headline that circulates in freelancer communities. The full picture always includes INPS.

5. Net income calculator: real numbers at every revenue level

The tables below show complete net income calculations for forfettario freelancers in 2026, using two common categories: a professional/consultant (78% coefficient, Gestione Separata INPS) and an IT/software professional (67% coefficient, Gestione Separata INPS).

Professional & consultant (coefficient 78%, INPS 26.07%)

| Annual revenue | Taxable base (78%) | Flat tax (15%) | INPS (26.07%) | Total deductions | Net income | Effective rate |

|---|---|---|---|---|---|---|

| €20,000 | €15,600 | €2,340 | €4,067 | €6,407 | €13,593 | 32.0% |

| €30,000 | €23,400 | €3,510 | €6,101 | €9,611 | €20,389 | 32.0% |

| €40,000 | €31,200 | €4,680 | €8,134 | €12,814 | €27,186 | 32.0% |

| €60,000 | €46,800 | €7,020 | €12,202 | €19,222 | €40,778 | 32.0% |

| €85,000 | €66,300 | €9,945 | €17,286 | €27,231 | €57,769 | 32.0% |

IT & software developer (coefficient 67%, INPS 26.07%)

| Annual revenue | Taxable base (67%) | Flat tax (15%) | INPS (26.07%) | Total deductions | Net income | Effective rate |

|---|---|---|---|---|---|---|

| €20,000 | €13,400 | €2,010 | €3,493 | €5,503 | €14,497 | 27.5% |

| €30,000 | €20,100 | €3,015 | €5,240 | €8,255 | €21,745 | 27.5% |

| €40,000 | €26,800 | €4,020 | €6,987 | €11,007 | €28,993 | 27.5% |

| €60,000 | €40,200 | €6,030 | €10,480 | €16,510 | €43,490 | 27.5% |

| €85,000 | €56,950 | €8,543 | €14,846 | €23,389 | €61,611 | 27.5% |

Figures use the standard 15% flat tax rate. Apply 5% in the first five years for substantially lower deductions. For exact calculations with your ATECO code, use the Paylio forfettario calculator.

One observation worth noting from these tables: the effective rate is constant at every income level within the same category. Unlike IRPEF — where the rate rises as income climbs — the forfettario produces a completely flat effective burden. A consultant earning €20,000 and one earning €85,000 both pay 32.0% of revenue in total deductions. This predictability is one of the regime's most practical advantages for financial planning.

6. Forfettario vs regime ordinario: which saves more?

The forfettario is not automatically the better choice for every freelancer. At higher income levels, or when you have significant legitimate business expenses, the regime ordinario — Italy's standard self-employment tax regime — can produce a lower tax bill.

Under the ordinario, your taxable income is your actual revenue minus your actual documented expenses. That income is then taxed under the standard IRPEF brackets (23%, 33%, 43%) and subject to INPS contributions. You also pay VAT and must maintain full accounting records.

The comparison depends on two variables: your revenue level and your expense ratio.

When forfettario wins:

- Your real business expenses are low relative to revenue (under ~30–35%)

- You are in the startup phase (5% rate makes the forfettario unbeatable)

- Your income is below €40,000 — at these levels, the ordinario rarely produces a better net

- You value administrative simplicity and lower accountancy costs

When ordinario may win:

- You have very high legitimate business expenses — software licences, subcontractors, equipment, office costs

- Your revenue consistently approaches or exceeds the €85,000 cap

- You have significant dependent family members whose deductions reduce your IRPEF bill under the ordinario

- You operate a business with a low ATECO coefficient (40%) but high actual margins — the ordinario lets you deduct real costs rather than being taxed on assumed 40% profit

Side-by-side at €60,000 revenue, consultant profile:

| Category | Regime forfettario | Regime ordinario (est.) |

|---|---|---|

| Revenue | €60,000 | €60,000 |

| Deductible expenses | — (not applicable) | €8,000 (assumed) |

| Taxable income | €46,800 | €52,000 |

| Income tax | €7,020 (15% flat) | €13,440 (IRPEF brackets) |

| INPS | €12,202 | €13,550 |

| Net income | €40,778 | €35,010 |

| Effective rate | 32.0% | 41.7% |

At €60,000 revenue with moderate expenses, the forfettario produces around €5,700 more net income per year. The gap widens further during the 5% startup period.

Use the Paylio freelancer calculator to toggle between forfettario and ordinario modes with your specific revenue and expense figures — the comparison is calculated in real time.

Compare Forfettario vs Ordinario

Directly compare your freelance take-home under different tax regimes in Italy.

7. Tax payment calendar: when do you pay?

Many new forfettario freelancers are caught off guard by Italy's advance payment system. You don't simply pay your annual tax bill once a year. You pay in three instalments.

- June — balance payment (saldo): Pay the full balance of the previous year's tax bill. This is the difference between what was actually owed and any advance payments already made.

- June or July — first advance payment (primo acconto): Pay 40% of the current year's estimated tax bill, calculated as 40% of last year's total. First-year freelancers with no prior year reference pay nothing here.

- November — second advance payment (secondo acconto): Pay the remaining 60% of the estimated current-year bill.

The result is that in June, you typically pay both the balance from last year and the first advance for the current year simultaneously — a double payment that surprises freelancers in their second year of activity if they haven't set aside funds throughout the year.

Practical advice: set aside approximately 33–35% of every invoice payment into a dedicated savings account throughout the year. This covers both the flat tax and INPS across all three payment dates without any cash flow surprises.

8. Frequently asked questions about regime forfettario 2026

What is the revenue cap for regime forfettario in 2026?

The maximum annual revenue is €85,000. If you exceed this in a given year, you transition to the regime ordinario from 1 January of the following year. If you exceed €127,500 in a single year (more than 50% above the cap), you exit mid-year immediately.

Can I switch from forfettario to ordinario voluntarily?

Yes. You can choose to apply the ordinario even if you qualify for the forfettario. This sometimes makes sense when you have high business expenses, significant IRPEF deductions as an individual, or are planning to grow past the €85,000 cap. Switching back to forfettario later is permitted subject to the standard eligibility criteria.

Do I pay VAT under the regime forfettario?

No. One of the most significant practical advantages of the forfettario is that you are exempt from VAT (IVA). You do not charge VAT on your invoices and do not file quarterly VAT returns. This simplifies administration considerably and is a genuine pricing advantage when billing to private clients or VAT-exempt organisations that cannot reclaim IVA.

How much does a commercialista cost under the forfettario?

Accounting fees for forfettario freelancers are typically €500–€1,500 per year — substantially lower than the €2,000–€5,000+ typically charged for ordinario accounts with full bookkeeping. Some freelancers with simple affairs manage tax filing independently using dedicated Italian tax software.

Does the forfettario affect my pension contributions?

Yes. INPS contributions under the forfettario count toward your Italian pension entitlement. However, because contributions are calculated as a percentage of your deemed (coefficient-reduced) income rather than full revenue, your pensionable earnings are lower than a salaried employee at the same income level. Many forfettario freelancers supplement with voluntary pension contributions (previdenza complementare) to compensate.

What happens if I exceed the €85,000 cap mid-year?

If you exceed €85,000 but stay below €127,500, nothing changes for the current year — you continue operating under the forfettario. From 1 January of the following year you switch to the ordinario. If you exceed €127,500 in a single calendar year, you exit the forfettario immediately and must apply ordinario rules retroactively from 1 January of that year, including issuing corrected invoices with VAT.

For more details, calculate your net position with our Italy Freelance Calculator or compare paths in the Salary Comparison Tool.